The Unlikely Winners: How did Europe’s FSCs become the market’s top equity performers in 2025?

With 2025 in the rear-view mirror, ExPlane analysed the share price performance of 15 listed airlines across Europe & the United States in the past 12 months. The performance of airlines differed based on business model and geography, with a few outliers.

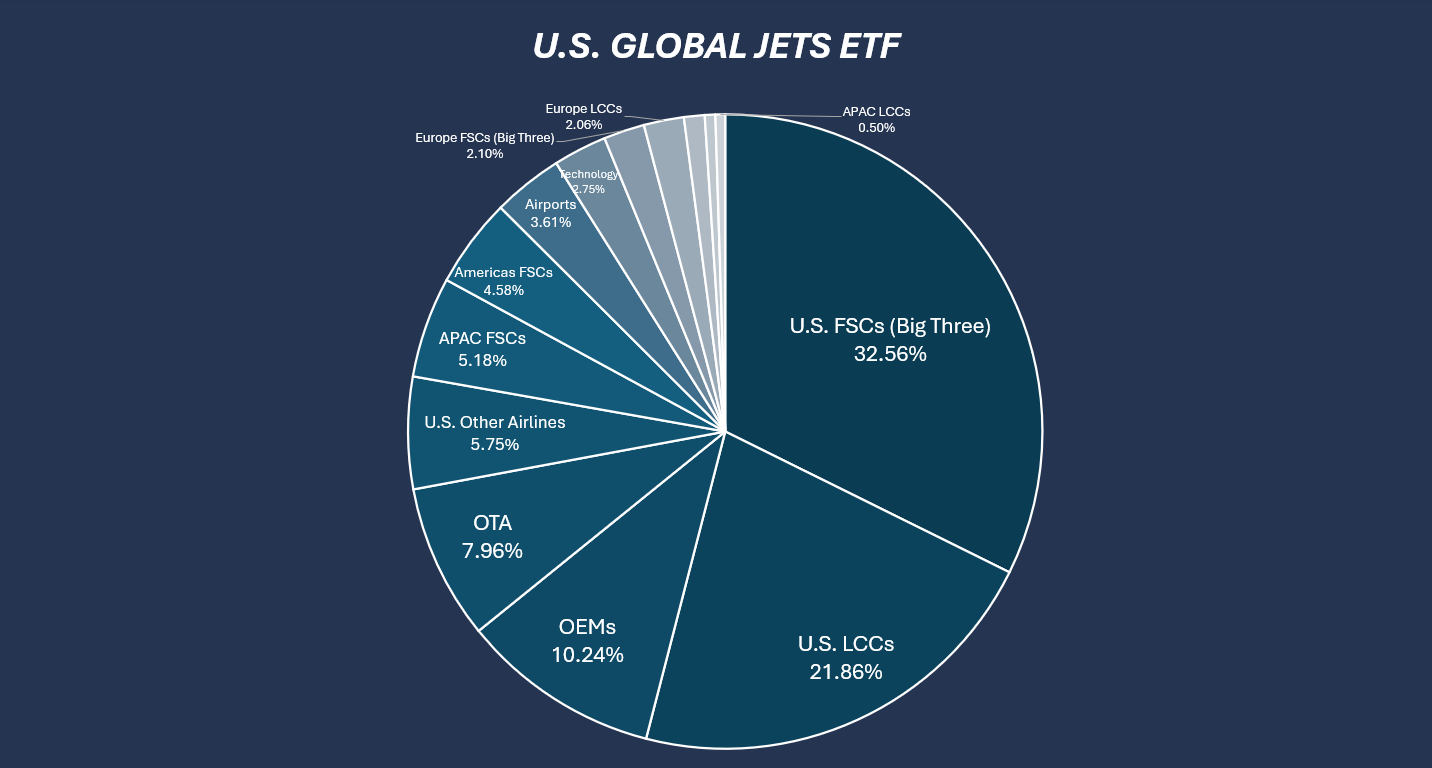

To understand airline equity performance in 2025, the ‘U.S. Global Jets ETF’ serves as a good starting point. As the name of the Exchange Traded Fund suggests, its composition is heavily weighted towards U.S. carriers, currently holding 60.17% of the fund. From the 10 U.S. carriers in the fund, United Airlines, Delta Air Lines & American Airlines represent more than half (32.56%) of U.S. airline equities. LCCs, represented by Southwest, Frontier, JetBlue, Sun Country & Allegiant, are slightly underrepresented, holding 21.86%. The balance (5.75%) is held by Alaska Airlines & SkyWest Airlines, which were omitted from the analysis below.

19 listed airlines outside the United States are held but only represent a cumulative 14.96% of the fund at the time of writing. The remaining 25.62% are held by non-airline equities including OEMs, Online Travel Agencies (OTAs), airports & technology companies.

United States…

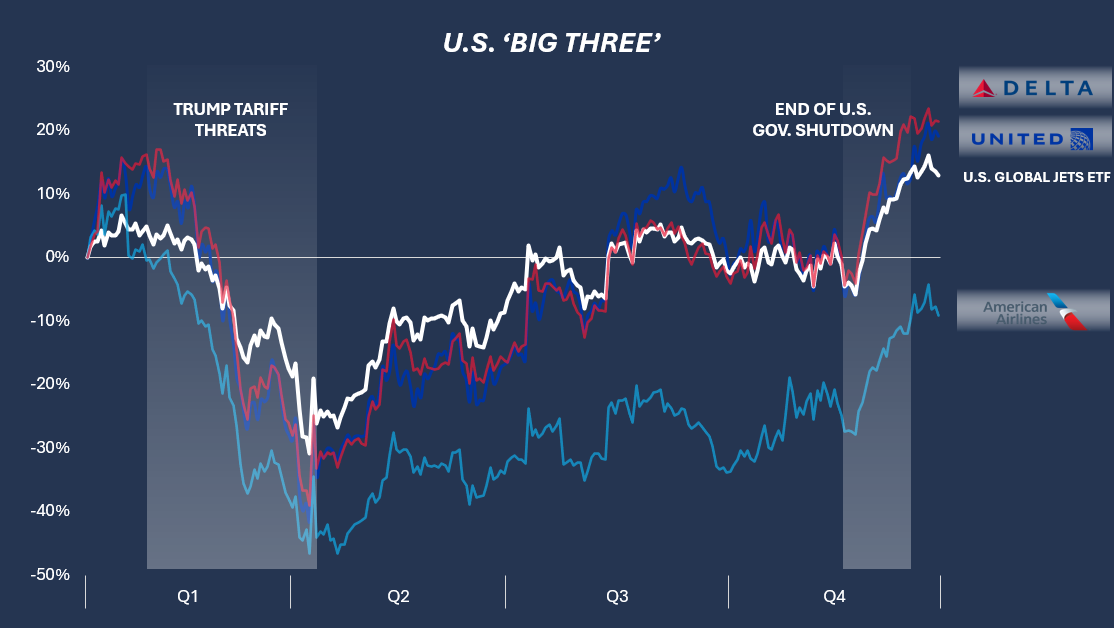

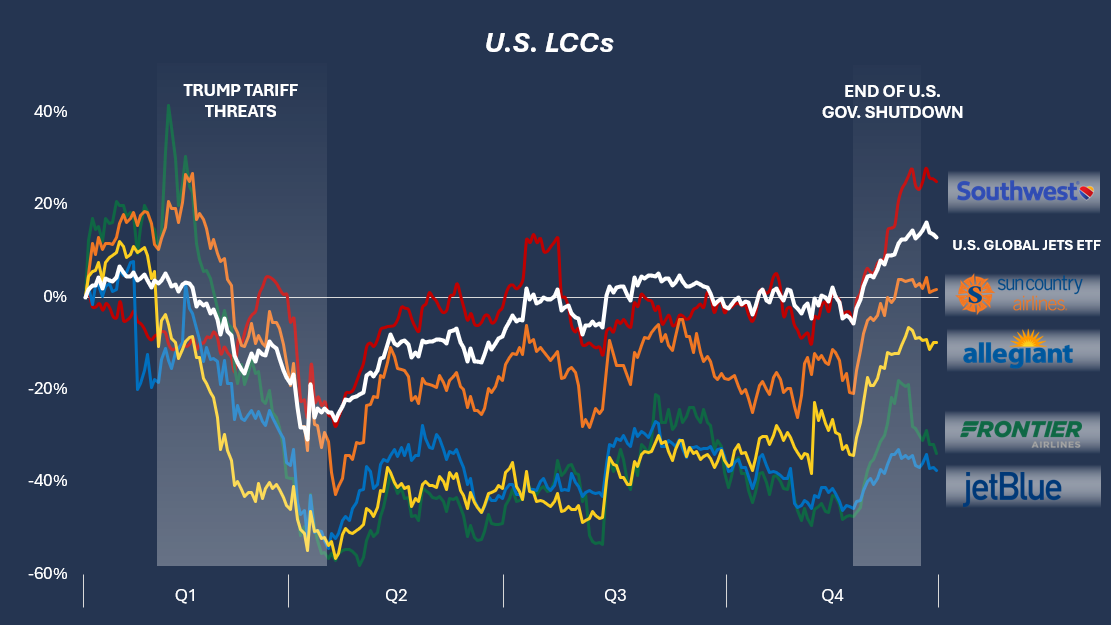

In the United States, both United Airlines and Delta Air Lines delivered strong shareholder returns of ~20%, with American Airlines falling short of its competitors and delivering negative returns of -9%. Despite the U.S. Global Jets ETF only holding 21.89% of United Airlines and Delta Air Lines equities, there is an evident link between the performance of the fund and both stocks. Southwest, which delivered a similar ~25% return and represents 10.79% of the fund, provides some additional reasoning as to why these airline equities and the fund moved in tandem. Together, these three airlines represent 32.68% of the fund.

Two notable events impacted the performance of U.S. airlines, irrespective of business model, throughout the year. During most of Q1 and into early Q2, recession fears loomed following the announcement of US President Trump’s widespread tariffs. Amidst this chaos, equity investors feared severe market dislocation due to debilitating tariffs on imported aircraft, declining consumer confidence (impacting forward bookings) and declining discretionary spending (eroding yields).

Many of these fears did not materialize anywhere near to the extent initially anticipated, with a widespread economic recession also being avoided. This, together with solid operating performance from Delta Air Lines and United Airlines in the first half of 2025, enabled full share price recovery by August. American Airlines notably lagged in this recovery, with equities hovering -30% to -40% from baseline (January 2nd, 2025) throughout most of 2025.

American Airlines’ issues have been subject to widespread coverage; much weaker financial results primarily stem from carrying significant legacy debt, as well as notable strategic missteps. The latter includes a less competitive hard product, especially evident in premium cabins, due to underinvestment, as well as hub overreliance (particularly DFW), which has made it more vulnerable to operational disruptions. Poor staff morale has also accentuated issues, impacting its soft product.

The second notable event occurred in November, when the U.S. government shutdown ended, triggering an industry-wide +25% correction amongst U.S. airline equities. The business model agnostic recovery (see graphs above & below) underlines that the rebound was solely driven by the promise of renewed operational stability following widespread flight cancellations due to ATC & TSA shortages during the shutdown, rather than the promise of rebounding government travel, strongly favoring FSCs.

As is well publicized, LCCs in the U.S. have struggled in the post-COVID market environment. This has forced Spirit Airlines to file for Chapter 11 in November 2024, making it the first major U.S. airline to file since 2011. The issues facing the LCC sector are multi-dimensional, with one of the most pressing challenges being the intensified competition from FSCs debundling their product and offering comparable no-frills economy options at similar prices, thus capturing price-sensitive travelers. An eroding cost advantage (especially pilot wage increases post COVID), market oversaturation (e.g. Las Vegas, Los Angeles, Orlando…), fleet reliability issues (e.g. PW GTF groundings) etc. have all been additional sources of headwinds.

Europe…

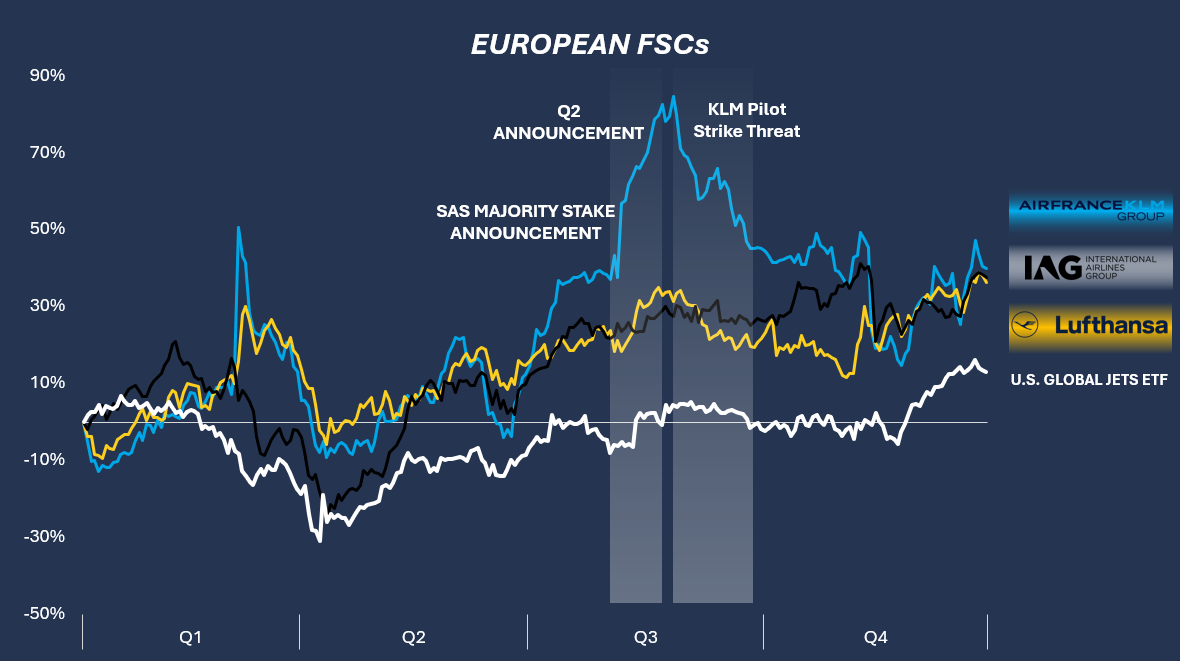

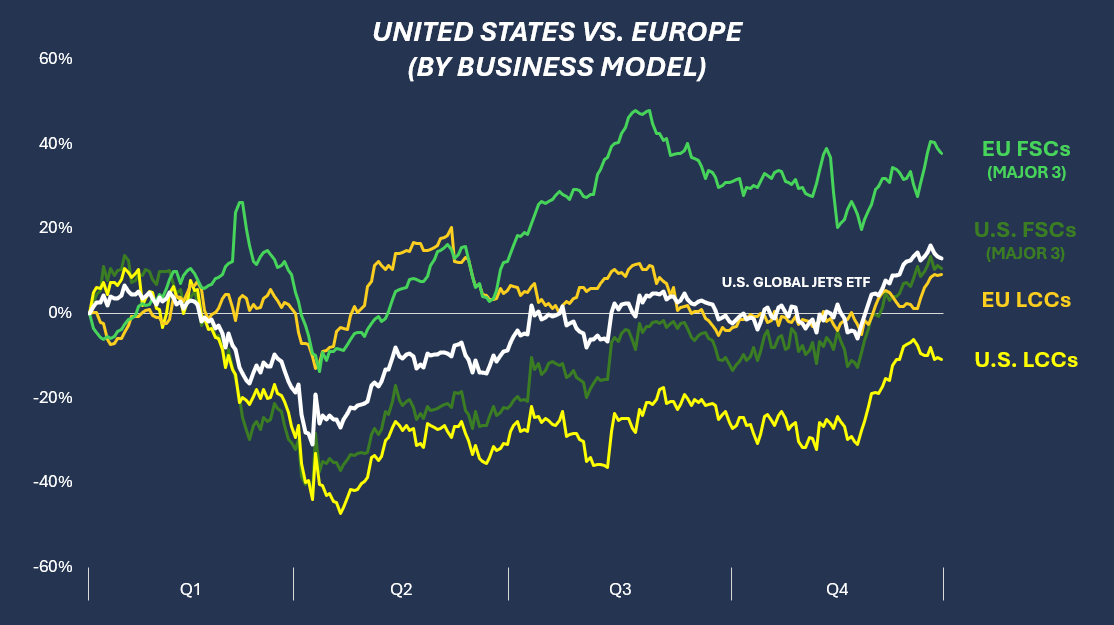

In Europe, the ‘Big Three’ airline groups, which include Lufthansa Group, International Consolidated Airlines Group & Air France-KLM, are only represented with 2.10% in the U.S. Global Jets ETF. The airline groups concluded the year with an almost identical return (~35-40%) to shareholders, outperforming the ETF by a factor of 4x.

The variable but overall positive airline results and outlooks had a minor impact to this impressive 12-month equity performance. The major tailwind underpinning this growth came from the low baseline in January 2025, in turn providing a longer runway for strong equity improvement. In fact, the share price of all ‘Big Three’ European airline groups continue to trade at a discount vs. pre-COVID, even with the impressive recovery witnessed in 2025. This is in strong contrast to the successful U.S. FSCs (Delta Air Lines & United Airlines), which trade above January 2020 levels.

Throughout the past year, Air France-KLM distinguished itself with heightened volatility, particularly evident in Q3. The spike, which commenced in late June, coincided with the Group’s announcement on July 4th that it had initiated proceedings to take a majority stake in SAS. The positive news continued with the Group’s positive Q2 2025 publication in late July, in which operating results improved by €223m y-o-y and margins expanded strongly to 8.7%. The subsequent fall was primarily due to KLM pilots threatening strikes over workload, while French unions were also discussing further action, raising fears of significant operational disruptions and increased labor costs. The strike was averted in late September, which is evident by the plateauing in the Group’s share price.

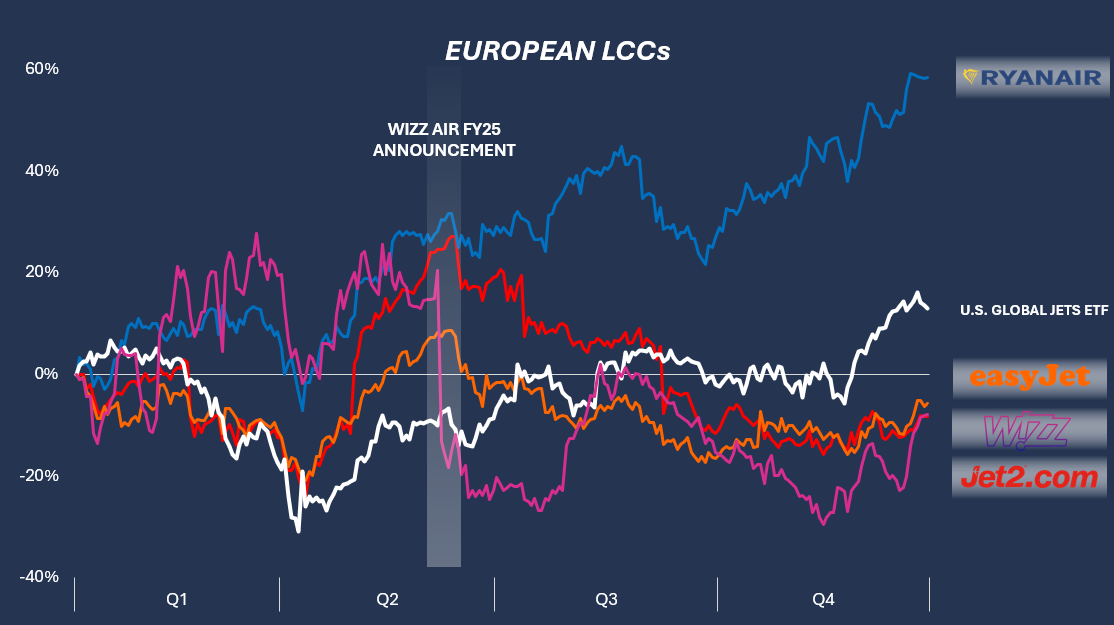

Amongst European LCCs, easyJet, Jet2.com & Wizz Air delivered negative shareholder returns which were contained to less than -10% by year end. Of the 15 airlines investigated, Ryanair was the stand-out performer with a 58.52% return.

Unlike European FSC equities, which continued to gain steady momentum throughout the year, the mid-year (end of Q2) signified a turning point in the fortune of European LCC equities. Whilst EasyJet & Jet2.com saw a gradual erosion, Wizz Air’s share price experienced an almost 40% free fall following the publication of its FY25 publication on June 5th in which the company reported a 61.7% drop in operating profit.

Today, Ryanair’s consistent profitability with double digit margins and a growing fortress balance sheet increasingly distinguishes it from any other LCC. On September 30th, 2025, the total shareholders’ equity stood at €8.97bn. The airline’s consistent share buyback program with a volume of €800m in FY25/26 and €750m in FY26/27 are testament to the airline’s strong performance and continue to provide tailwinds for strong share price appreciation.

The investigated U.S. FSCs & LCCs, which represent 54.42% of the U.S. Global Jets ETF, both underachieved the fund’s overall performance, suggesting that the balance comprised of non-airline equities (25.62% of fund), non-U.S. airline equities (14.96% of fund) and Alaska Airlines & SkyWest Airlines (5.75%), on a cumulative basis outperformed the investigated U.S. airlines.

Conclusion…

Analyzing airline stocks on an annual basis, in isolation of wider trends, has its limitations. However, this level of granularity provides clear insights into how annual events (e.g. financial report announcements, consolidation, strikes, macro-economic uncertainty etc.) impact airline equities for short-sighted investors.

Following years of underperformance, European FSCs strongly outperformed their counterparts in the United States, as well as the investigated LCCs on both sides of the Atlantic. Looking into 2026 and the second half of the decade, equity performance tailwinds - primarily in the form of continued airline consolidation (e.g. TAP Air Portugal) - will be challenged by tailwinds, especially in the form of cost pressures arising from environmental costs (e.g. EU ETS & SAF mandates) and broader labor cost inflation, creating a mixed outlook.