Lessor Risk Management amidst Geopolitical Tensions: China

Russia’s invasion of Ukraine in February 2022 highlighted the risks that lessors face when leasing aircraft into geopolitically fragile jurisdictions. Over 400 leased aircraft worth $12bn ended up stranded in Russia, with slim prospects of repossession and uncertainty on whether courts would vote in favor of the subsequent lessor insurance claims.

Through Russia’s unprovoked aggression towards Ukraine, the perceived threat level of similar altercations in other parts of the world heightened exponentially. In this context, China’s territorial claims over Taiwan have been of particular concern. After all, if Russia can execute a brazen and rather uncalculated act of territorial expansion, why would China not be capable of doing similar?

Unsurprisingly, the geopolitical tensions outlined above have had profound implications on how international lessors manage country concentration risk. The following graphs and commentary provide more detailed insights:

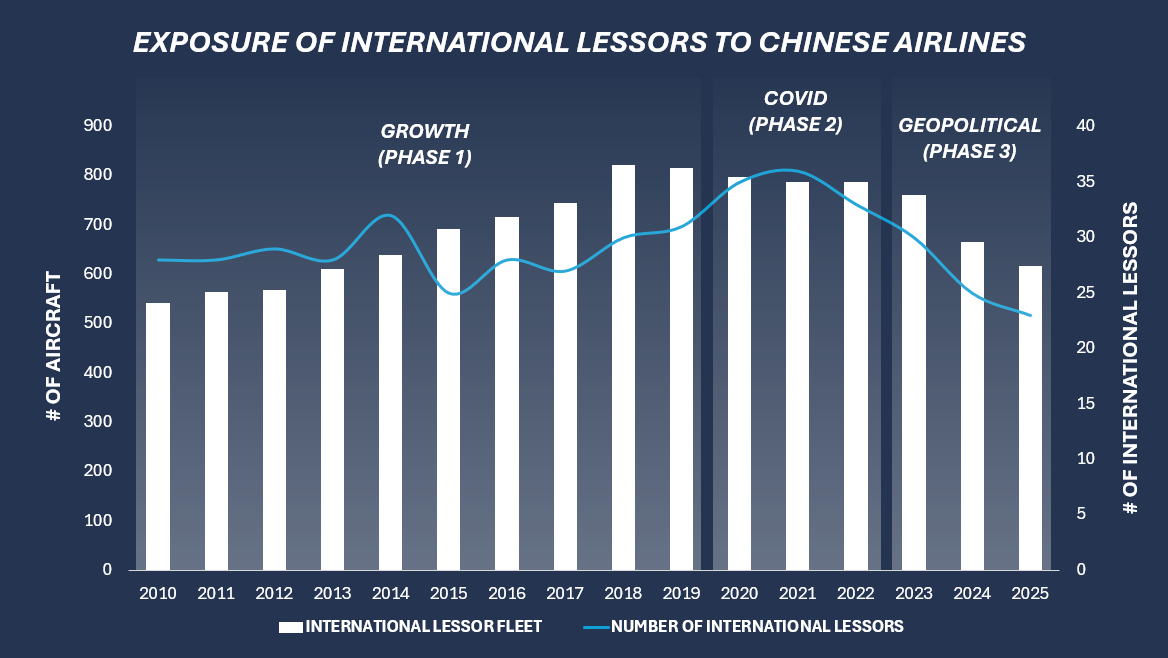

Amidst the boom in Chinese air travel demand, international lessors progressively expanded their exposure to Chinese airlines in the 2000s & 2010s. Cirium data suggests that exposure increased by over 50% from 543 aircraft to 821 aircraft in the 2010s (Phase 1). Unsurprisingly, the COVID pandemic stalled this growth, with lessor exposure flatlining at roughly 800 aircraft (Phase 2).

Russia’s invasion of Ukraine in February 2022 instigated a sustained decline of roughly 200 aircraft in the ensuing 3-year period (Phase 3). Today, the international lessor fleet size stands at 2013 levels. To proactively manage risk, and reduce exposure aggressively, lessors traded aircraft to local lessors, stopped originating new leases and refrained from extending expiring leases.

Many international lessors also exited China altogether. In the past three years, 13 companies have taken this drastic measure, leaving only 23 international lessors exposed to Chinese airlines. This is significant, as it suggests that less international lessors have exposure to China than in 2010.

The true magnitude of exposure reduction is likely much higher than portrayed in the chart above. All entities that have their headquarters registered outside of China were considered ‘international lessors‘, even if the parent company is Chinese. As a result, Chinese controlled entities such as CDB Aviation (Ireland) and BOC Aviation (Singapore), are considered international lessors for the purpose of this analysis. The Cirium data confirms that said entities have not reduced their China exposure to the same extent compared to truly international lessors.

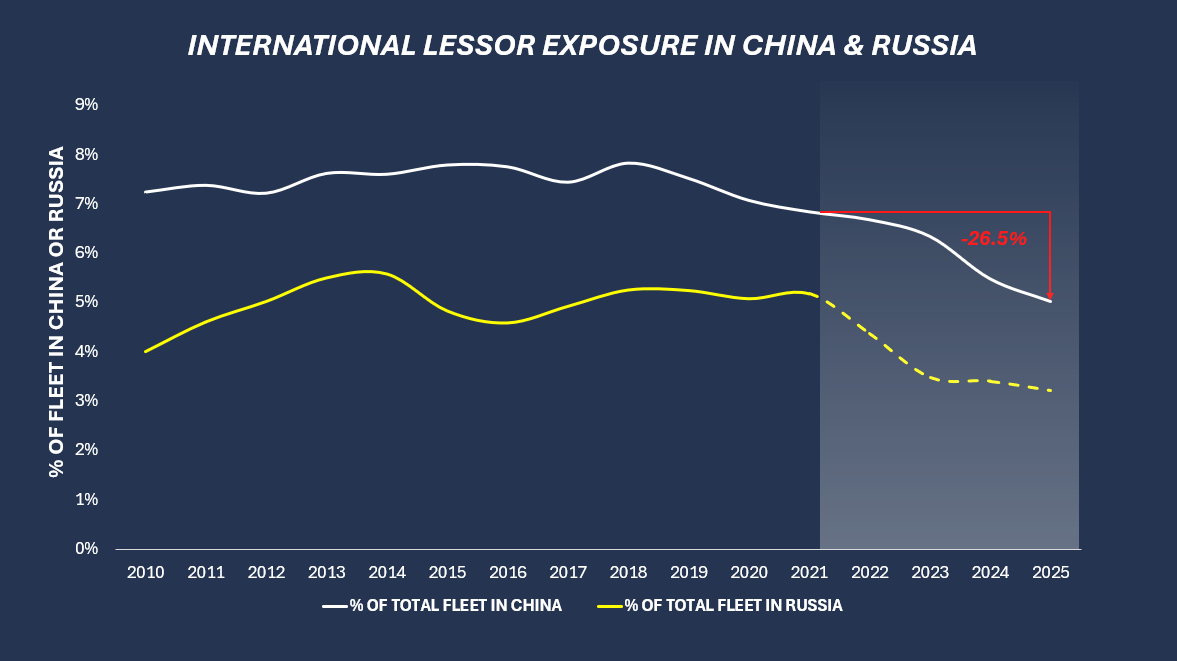

The impact of international lessors downsizing country concentration is also evident through the chart above. In the 2010s, non-Chinese lessors placed between 7-8% of their total portfolio (by number of aircraft) with airlines in China. As the Chinese airline fleet grew, so did (in proportional fashion) the international lessor fleet.

Since the onset of the Russia-Ukraine war, this exposure has reduced markedly to only 5.03% of their global portfolio. In contrast, it is evident that international lessors undertook no action to reduce their portfolio concentration in Russia, which hovered between 4-5%, up until Russia’s invasion of Ukraine. As such, it is evident that lessors did not foresee the geopolitical fallout that would ensue. Based on their proactive portfolio downsizing in China, it is apparent that lessors have become more attune to geopolitical risks in the wake of Russia’s aggression.

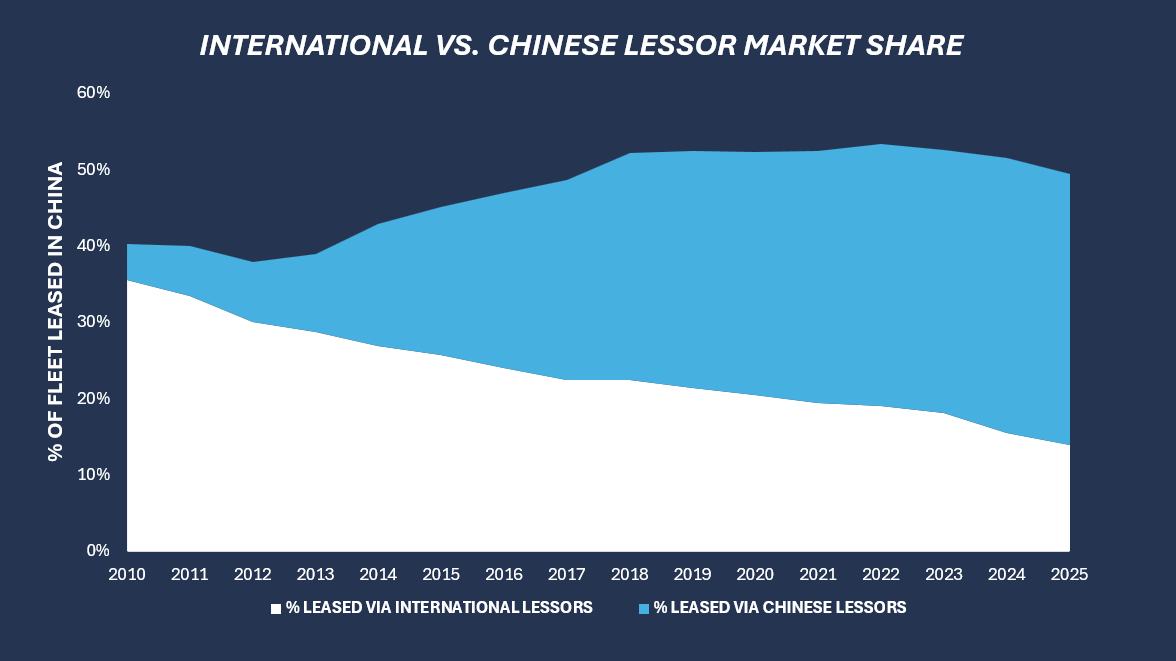

Holistically, the Chinese leasing market has tracked global trends. For example, the percentage of leased commercial aircraft has steadily grown from 40% to 50% over the past 15 years.

However, as evidenced in the chart above, the composition of lessors doing business in China has radically changed. In the investigated timeframe, Chinese lessors have significantly grown their domestic market share. In 2010, only 5% of commercial aircraft operated in China were leased through a Chinese-headquartered entity. Today, this figure stands at 35%. In contrast, the market share of international lessors has reduced from 36% to 14%. The growing support of Chinese leasing companies for their national airlines is also clearly visible in the chart below.

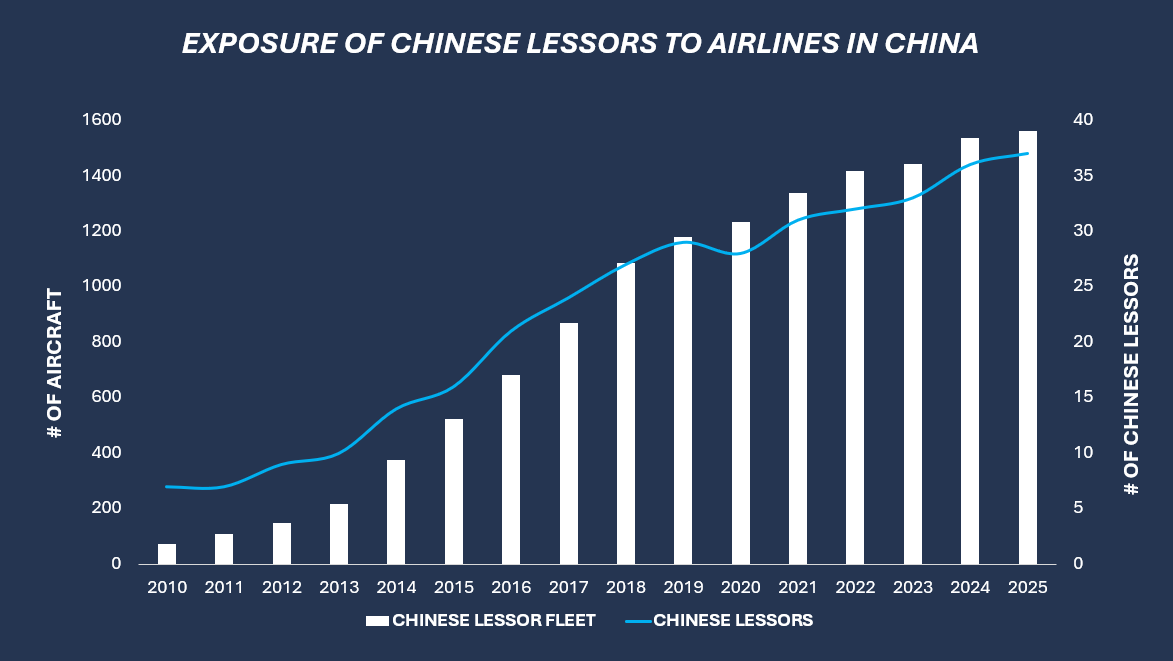

The unabated growth of Chinese lessors has led to 37 entities leasing 1’561 aircraft to airlines across China in 2025.

Amidst continued caution & potential further contraction amongst international lessors, it is expected that the role of Chinese lessors will continue to strengthen even further as Chinese airlines look to finance their next wave of fleet modernization and growth. It remains to be seen at what level of exposure international lessors will plateau, and to what extent the global leasing community is willing to forfeit growth prospects in the world’s second largest aviation market.