The Equilibrium of Lessor OEM Orderbooks

Lessors can grow their portfolios through four channels: Speculative OEM Forward Orders, Sale-Leasebacks (SLBs), Trading and M&A.

Speculative OEM forward orders have long played an important role, with all stakeholders directly involved benefiting in different ways:

𝗟𝗲𝘀𝘀𝗼𝗿𝘀: Provides a steady stream of deliveries enabling both growth visibility and growth certainty, an important element that the other three channels above are unable to provide. Moreover, the company holds a delivery slot which (as the delivery approaches) would otherwise not be available to airlines, enhancing its value.

𝗢𝗘𝗠𝘀: Provides a predictable base of annual deliveries to companies with very strong credit metrics & large existing customer bases. This minimizes the risk of deferrals or cancelations.

𝗔𝗶𝗿𝗹𝗶𝗻𝗲𝘀: Provides access to a delivery slot which would otherwise not be available, enabling operators to be more flexible and opportunistic when committing to fleet growth.

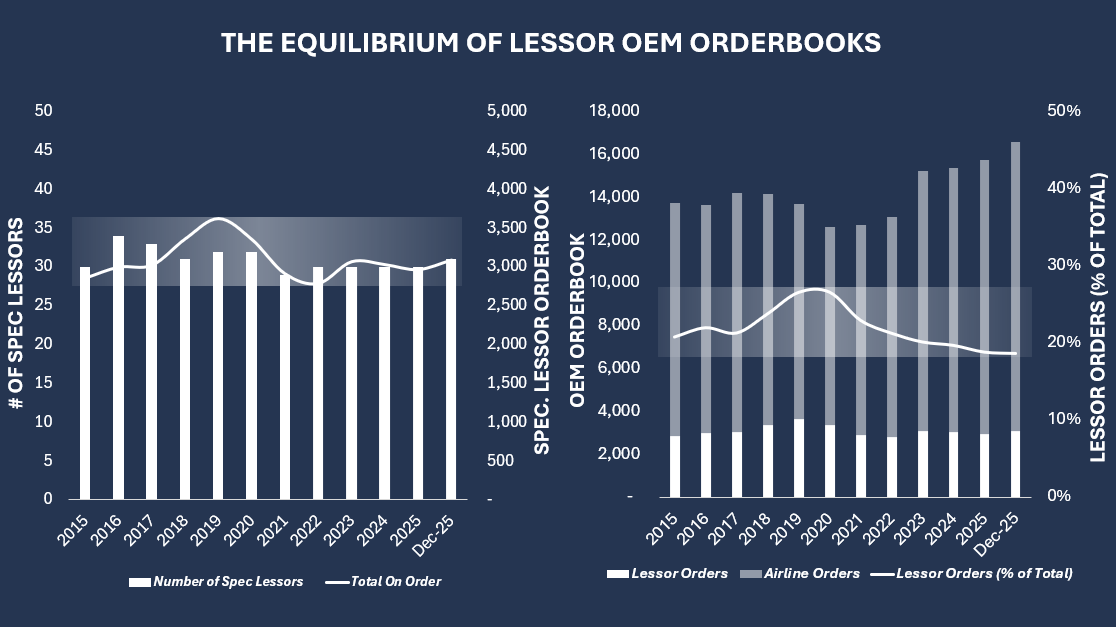

Despite the above, the size and scope of speculative lessor forward orders is tightly controlled by OEMs. Data from the past 10 years paints a clear picture:

𝗡𝘂𝗺𝗯𝗲𝗿 𝗼𝗳 𝗟𝗲𝘀𝘀𝗼𝗿𝘀: There has been a steady stream of roughly 30 lessors with open forward orderbook positions at any given time. This is not by coincidence, as OEMs look to sell to well-established, highly credit-worthy lessors with low cost of capital and a strong track record (incl. large customer bases). These high barriers to entry disqualifying many lessors and, in the eyes of the OEM, maximize placement success. For competitive friction, OEMs will look to have a handful of lessors (3-5) on each aircraft program. With up to 10 aircraft programs selling at any given time (across Airbus, Boeing, Embraer & ATR), and many speculative lessors opting to execute forward orders on more than one program, a natural equilibrium of 30 lessors is formed.

𝗡𝘂𝗺𝗯𝗲𝗿 𝗼𝗳 𝗢𝗿𝗱𝗲𝗿𝘀: Lessors have held roughly 2,800 – 3,600 orders at any given time, holding between 19-27% of the total OEM orderbook. Allocating one-in-four to one-in-five slots for lessors is the equilibrium of choice for OEMs, as it balances the following forces: (i) providing a majority of slots to airlines - its ultimate end-user, (ii) providing a meaningful number of slots to lessors that will, by in-large, pay more for a slot than the airline, (iii) providing a meaningful (and in the current environment similar) amount of slots for the SLB market, appeasing both airlines and the wider leasing community.